CMS moves a little on rate hike for plans given troubled finances and beneficiary impacts

The Centers for Medicare and Medicaid Services (CMS) has released its Final Announcement for calendar year (CY) 2027 rates and policies for Medicare Advantage (MA) and Part D. I wrote about the Advance Notice back on January 29. I will not repeat much of the technical explanations again here, but please go back to that blog for in-depth explanations of various rate-setting terms.

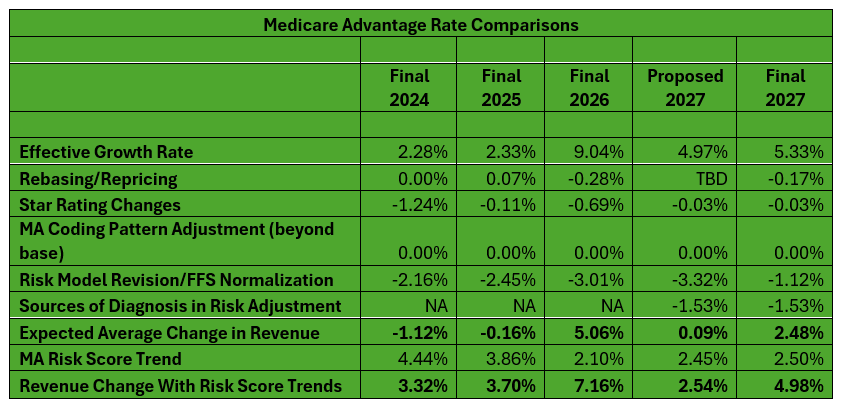

Proposed rates tend to increase each year between the Advance Notice and Final Announcement as more data is updated from the fee-for-service (FFS) program. The plan benchmarks are based on both FFS and MA costs. Based on past history, I had predicted that rates would end up between 2% and 3% as the Effective Growth Rate (EGR) would increase markedly between the advance and final notices. In the end, the EGR actually did not increase much in the two plus months — just 0.36%. But rates before risk score trends will go up by 2.48% (vs. 0.09% in the Advance Notice) because CMS will not implement further changes to the v28 risk model for CY 2027 that were proposed in the Advance Notice. This is well below the over 5% hike this year.

CMS had proposed to update the Part C risk adjustment model using more recent underlying original Medicare data (updated from 2018 diagnoses and 2019 expenditures to 2023 diagnoses and 2024 expenditures). This would recognize more current costs. Instead, for CY 2027, CMS will continue to use the 2024 MA risk adjustment model which was calibrated with original Medicare 2018 diagnoses and 2019 expenditures data that was fully implemented in CY 2026. The nearly 2.5% hike will mean about $13 billion in additional payments to plans in 2027. Some argue the trends really are closer to 5% given risk score trends are at about 2.5% overall as well. But I side more with plans on this – risk score trends are not free revenue and are reflective of rising risk. And if there was fat in risk score trends from year to year, that has changed with v28. The 2.5% projected overall risk score trend is well below past trends.

Why did CMS change its mind on the further v28 model change, which would have impacted all plans to the tune of 2.2%? Probably three reasons. From a policy perspective, plans argued that the acceleration of the data in the model would represent costs inaccurately. From another policy standpoint, CMS likely worried that a near-zero hike would be destabilizing after the 3-year phase in of the v28 model, which has taken over 7% out of rates. Last, from a political perspective, the paltry 2027 hike would have led to a fourth year of contraction geographically as well as from a product and benefits perspective. That would mean higher premiums, greater cost-sharing, and slimmer benefits would be advertised right before the mid-terms.

On the first point on cost recognition, while CMS decided to push off the latest model change, it is hard to agree with the plans’ position. While there are some oddities right now in the FFS program, generally speaking the model should represent the latest costs as much as possible.

On the second policy point, CMS noted that MA plans were hit by the impacts of the v28 model from 2024 to 2026. By my calculation, that took 7.62% out of rates with normalization. CMS’ move is a small recognition of the churn and volatility in the industry right now. CMS officials say that the final approach aims to balance immediate challenges in the program with the agency’s goals of promoting long-term stability for MA. CMS said the decision on updating the v28 model is indefinite and it is monitoring plans.

The agency said it is still focused on addressing insurer behavior on risk adjustment upcoding and overpayments. Therefore, it is finalizing the exclusion of diagnoses from audio-only encounters and diagnoses from chart reviews not linked to actual encounters, with an exception to include diagnoses from unlinked chart reviews for beneficiaries who switch from one MA organization to another. Insurers lobbied hard for this.

The industry is not happy as the hike is still very low in a very high utilization environment. Frankly, I am surprised that the EGR update was just 0.36% in such a high utilization environment.

And as I noted, the chart changes do not impact the industry equally. The largest plans are disproportionately impacted given their aggressive risk adjustment coding practices. Experts say UnitedHealthcare faces a $5 billion reduction and Humana $2 billion. So, a case can be made that most plans will see a rate hike of about 4%.

The impact overall

This is a repeat of what I published in the January blog, but it bears scrutiny. In the next table, I go further on the troubles MA plans have seen and will see. The industry came off of high annual rate hikes early in the 2020s. In 2024 and 2025, these hikes were basically zeroed out due to the risk model change and low effective growth rates. Compounding the problem was a major drop in Stars starting with 2023 ratings and running so far through 2025 ratings. On the cost side, utilization and other trends (such as drug costs) leapt coming out of COVID. As well, CMS has placed new costly burdens on plans, including requiring them to follow FFS prior authorization processes (I say taking the managed care out of managed care) and new unpaid costs from the Inflation Reduction Act’s (IRA) Part D cost-sharing changes. All this created a perfect financial storm for MA plans. MA plans say they are digging out. They used 2024 (to some degree) as well as 2025 and 2026 to right the financial ship. But the 2027 rate news, even with the uptick in the final announcement, likely means some further geographic, product, and benefit contraction in 2027.

In the end, the Final Announcement has a mix of good news, bad news – some relief but continuing anxiety – for plans.

On Thursday I will update on some of the Star updates in the Final Announcement.

| Medicare Advantage’s Rocky Stars, Rates, and Medical Expense Road | ||||||

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | |

| Star scores (score impacts the following calendar year revenue) | Very High (impacts 2023 revenue) | Scores dropping — first year of recent drop (impacts 2024 revenue) | Scores low – second year of recent drop (impacts 2025 revenue) | Scores low – third year of recent drop (impacts 2026 revenue) | Scores low – marginally higher than 2025 (impacts 2027 revenue) | TBD – to be announced in October 2026 (impacts 2028 revenue) |

| Rates | Very High | High | Low | Low | Somewhat Low | Low |

| Medical Expense | Rising | Rising | High | High | High | High |

#medicareadvantage #rates #2027

— Marc S. Ryan