A quick blog to tell you about enrollment growth in Medicare Advantage (MA) in both October and November 2025. The October data was delayed due to the government shutdown. Recently, both the October and November data were posted. Due to the financial meltdown of health insurers in general and in the MA line specifically, many of the biggest plans have sought to restrain growth. But growth has continued throughout the year because of some strong benefit packages still out there and the better value in MA compared with traditional fee-for-service (FFS) Medicare. We are now in open enrollment for 2026 so we will continue to see growth in Q4 2025 because of some enrollees who are able to switch early (before January 2026) with special enrollment periods.

What do the latest statistics show?

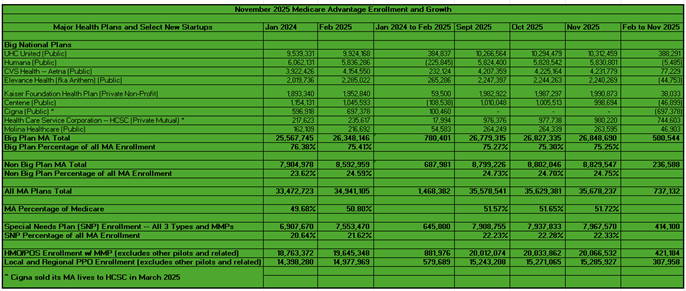

Growth from January 2024 to February 2025 was 4.39% or 1.468 million. (I used February 2025 because of issues with the January 2025 statistics.) Enrollment in MA reached 34.941M in February 2025. In November 2025, it reached 35.678M, growing 100K since September. MA enrollment grew about 49K from October to November and about 737K from February to November.

How did Big MA do?

From January 2024 to February 2025, Big Plan MA enrollment performed very poorly because of retrenchment among some of these plans. Big MA grew by about 780K or 3.1%. Big MA enrollment hit 26.348M. This compares with about 688K growth or 8.7% for all other MA plans. All other MA plans grew to 8.593M in February 2025.

Big MA’s penetration dropped from 76.4% in January 2024 to 75.4% in February 2025. Big MA has grown about 501K lives from February to November 2025, or about 68% of growth in that timeframe. This trails Big MA’s overall penetration. Big MA growth in October was 48K and 22K in November. Non-big MA plans grew just 3K in October and 27K in November.

United Healthcare grew by about 28K in October 2025 and 18K in November 2025. United has grown about 388K since February. Because of United’s major financial troubles, United announced it is terminating most MA commissions as of July 1. This was supposed to help stem additional growth throughout the rest of 2025. But it is still growing. It clearly does not want to grow given its financial condition but continues to have the best benefits in 2025 for large MA plans.

Humana grew by about 7K from September to November and has contracted by about 5K since February. Humana is said to be doing well among the big plans for 2026 signups for January 1.

CVS grew by about 18K in October and 7K in November. It has grown about 77K since February. It also does not want to grow due to its efforts to right its financial ship, but enrollees have been attracted to its benefits despite its pullback.

Elevance Health, another plan cutting commissions, contracted by 7K from September to November and has dropped about 45K since February.

Kaiser grew by about 8K from September to November and 38K since February.

Centene dropped by about 11K from September to November and about 47K since February.

In March, Cigna closed its sale of its Medicare assets, including its over 700K MA lives, to Health Care Service Corporation (HCSC). As such, HCSC jumped from about 239K in March to 957K in April. It is now the 7th largest MA player. It grew by about 5K in May, 3K in June, 3K in July, 5K in August, 4K in September, 2K in October, and 2K in November. It now has about 980K members.

Molina is about flat from September to November, but has added about 48K since February (almost entirely due to its acquisition of ConnectiCare).

Special Needs Plans chugging along

Special Needs Plans (SNPs) (including retiring MMP demonstrations) continued to see a healthy increase in enrollment. From January 2024 to February 2025, SNPs grew to 7.553 million, a gain of about 646K or 9.35%. SNP enrollment grew about 264K in the enrollment season. But this growth is still down from the January 2023 to January 2024 period. In that period, SNPs added 1.154 million or 20.1%.

SNPs grew an amazing 102K from May to June. SNPs added another 42K from June to July and yet another 42K from July to August. From August to September, SNPs grew about 26K. SNPs grew about 29K from September to October and about 30K more from October to November. From February to November, SNPs added 414K more lives. SNP growth is about 56% of all MA growth from February to November. Including enrollment season growth through September, SNPs have grown about 678K.

PPOs vs. HMOs

Over the years, PPOs began growing and competing well with HMOs in terms of raw numbers as well as percentage growth. While PPOs’ sheer number and percentage growth was beating HMOs over the past several years, that trend changed from January 2024 to February 2025. From January 2023 to January 2024, HMOs grew about 853K (4.8%) and PPOs 1.861 million (14.8%).

But from January 2024 to February 2025, HMOs grew more than PPOs in terms of numbers and percentage: HMOs up about 882K (4.7%) vs. PPOs up about 580K (4%). HMOs grew by about 480K during the enrollment season, while PPOs contracted by about 58K.

From February to November, HMOs grew by about 421K while PPOs grew by 308K. From August to September, though, surprisingly HMOs grew by about 21K compared with 29K for PPOs. The same held true from September to October, where HMOs grew by about 22K while PPOs grew by about 28K. But from October to November, HMOs grew by about 33K while PPOs grew by just 15K. Plans have cut PPO offerings dramatically for 2026.

#medicareadvantage #enrollment #cms #healthplans #coverage

— Marc S. Ryan