Congress should take note of a report that rips apart MedPAC’s sometimes biased analyses

In my March 9 blog on the great exaggeration of the death of Medicare Advantage (MA), I told you about a recent opinion piece by former Health and Human Services secretaries Donna Shalala and Tommy Thompson supporting MA and questioning analyses by congressional Medicare policy arm MedPAC. In it they refer to the Healthcare Leadership Council’s (HLC) September 2025 report that literally ripped apart the government advisory entity’s MA analyses.

For years, I have been saying MedPAC as well as many academics have clear anti-MA bias. Their analyses are flawed and use old data to confuse the public and lawmakers. I have cited studies that stand in stark contrast to these biased analyses. But the HLC’s report, titled “Setting the Record Straight: The Fact’s Behind MedPAC’s Misleading Cost Analysis of Medicare Advantage,” is perhaps the most in-depth and forceful of any I have seen. As such, I wanted to devote today’s blog to the report. The full report’s link is at the end of this blog.

The damage MedPAC’s erroneous overpayment report causes

Before we get to the HLC report, I wanted to outline the ongoing problem. MedPAC continues to promote its bad data. In its just released report to Congress, MedPAC pegged the overpayment at 14% greater than traditional Medicare fee-for-service (FFS). This includes 4% for actual risk adjustment (which is well down from before due to the v28 risk adjustment model adoption) and 10% for favorable selection. MedPAC says the 14% means an extra $76 billion for MA each year. A separate analysis by Trump administration officials says the risk adjustment overpayment is just 2%, and that could go down further with proposed v28 model changes for 2027. As I have always said, the favorable selection analysis is extremely dubious. As the Better Medicare Alliance noted before MedPAC’s report was formally issued: “MedPAC estimates do not accurately reflect Medicare Advantage spending, nor do they even attempt to capture the superior value of the program to beneficiaries and taxpayers. That is a problem.” Well said.

But the bad data from MedPAC continues to cause problems for MA plans. It has led yet another congressional committee to issue a scathing attack on MA using MedPAC’s flawed numbers. The bipartisan congressional Joint Economic Committee (JEC) concluded that overpaying for MA plans caused Medicare Part B premiums to rise across the board. It says the overpayments caused standard monthly Medicare Part B premiums to go from $185 in 2025 to $203 in 2026. The JEC defined “overpayments” as the difference between what the federal government paid for MA plans versus traditional Medicare. It cited MedPAC statistics that MA plans were paid $84 billion more (an earlier overpayment number) than it would have cost to cover the same amount of beneficiaries with traditional Medicare. The report urged action. “Today, between aggressive upcoding, questionable quality bonuses, and structural overpayments in Medicare Advantage, seniors who stay in traditional Medicare are effectively subsidizing the system. That’s not sustainable, it’s not fair, and it can be reformed,” said Chair Rep. David Scweikert, R-AZ.

The HLC report’s findings

As I said, the HLC report is perhaps one of the most comprehensive pushbacks on the MA overpayment narrative I have seen out there. Here are the key points from the HLC report:

- HLC notes that in 2024 MedPAC adopted a new methodology that incorporates a flawed approach for estimating coding intensity and, for the first time, added a questionable, separate estimate for calculating “favorable selection.”

- The report notes that MedPAC’s new methodology nearly quadrupled MedPAC’s 2023 overpayment, moving it from 106% to 121%.

- MedPAC also retrospectively applied the new methodology to recalculate previous overpayment estimates for MA from 2007 to 2023.

- MedPAC relies on traditional Medicare as the neutral coding benchmark despite known undercoding in FFS. In a transactional payment system, traditional providers have little incentive to document all diagnoses because one appropriate diagnosis will get a claim paid and adding more is an administrative burden. As HLC notes, the structural undercoding means the FFS baseline is systematically lower than true patient complexity. Thus, using FFS as the benchmark inflates any overpayments in MA.

- Although not advertised, MedPAC’s analysis does find MA and FFS payments were essentially identical at 100% in 2024 and 2025 before MedPAc’s machinations.

- MedPAC’s incorporation of the untested demographic estimate of coding intensity (DECI) methodology more than doubled its estimate of coding intensity in recent years. MedPAC had earlier rejected DECI’s adoption. The report says MedPAC “conflates differences in health status with coding behavior. An accurate estimate should isolate differences in diagnostic coding between MA and FFS, not differences in underlying population health.”

- HLC also says that MedPAC inadequately accounts for the new MA risk adjustment model, which fails to recognize the plateau of coding intensity that is occurring and will continue to occur.

- HLC says that “significant differences in benefits, populations served, care delivery, and payment models between MA and FFS make direct spending comparisons misleading without adequate context.”

- The report cites a Milliman analysis that finds that MA delivered $185 per member per month in additional value ($59.9 billion in 2024) and that government spending on MA was modestly lower (4%) compared to the traditional program. Further, beneficiary costs were nearly a third (29%) lower than FFS.

- The report also notes an FTI Consulting analysis that identified flaws in MedPAC’s data and assumptions on favorable selection. Flaws included an over-reliance on “switchers” (beneficiaries who moved from FFS to MA); the exclusion of key groups in the analysis (ESRD kidney, Part A only, and secondary payer populations) and not accounting for differences between dual-eligible and Special Needs Plan (SNP) members and traditional populations. Further, MedPAC did not incorporate plan bids into its cost analysis.

- The report notes a Harvard Medical School and Inovalon analysis that contrasted with MedPAC’s assumption that lower-cost beneficiaries disproportionately select MA. That assumption drove the favorable selection overpayment finding. The Harvard and Inovalon finding was that, immediately prior to enrollment, MA enrollees are modestly less sick than their FFS enrollee counterparts (with about 10% lower risk scores).

- In determining favorable selection, HLC says MedPAC’s analysis is based on data from just 38% of all MA enrollees. MedPAC only analyzed the costs of MA beneficiaries who were previously enrolled in FFS for at least two full years. Further, MedPAC ignores the increasingly diverse and medically complex populations enrolling in MA. HLC says that MedPAC “ignores the likelihood that, as more beneficiaries enroll in MA initially, average costs will increase, particularly due to increasing enrollment of beneficiaries who are dually eligible or have ESRD.”

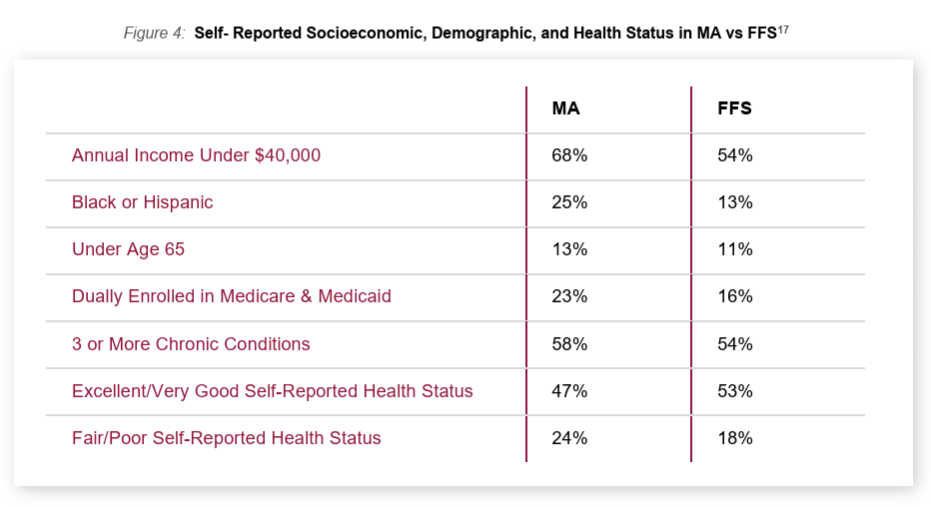

- Figure 4 of the HLC report below shows that MA enrolls lower income, more diverse, and more medically complex populations than FFS. Further, as of 2021, MA had a majority of dual eligibles. HLC says the increased enrollment of individuals with complex care needs runs counter to MedPAC’s premise of favorable selection in MA. It notes that those with ESRD are not included in the MedPAC analysis.

- MedPAC does not include any MA encounter data in its analysis, arguing it is incomplete. It instead uses “an indirect, roundabout approach, comparing the costs of beneficiaries who stay in FFS with past data of FFS beneficiaries the year before they switched to MA.”

- The report says that “estimates derived from incomplete data and flawed assumptions can quickly take hold, improperly shaping perceptions of MA’s value and potentially driving reforms that ultimately harm both beneficiaries and providers.”

- A key conclusion on favorable selection was outlined by the report as well. Here is the verbatim point made by HLC.

“Many beneficiaries join MA because out-of-pocket-costs in FFS hinder their ability to afford necessary care. Enrolling in MA may ultimately improve beneficiaries’ ability to access care due to additional benefits available, such as consumer protections that cap out-of-pocket costs, care management for chronic conditions, and medical transportation services. As a result, after joining MA, a beneficiary’s healthcare use and spending may naturally increase with more affordable access to necessary care. If MedPAC considered how MA improves access to care for unmet health needs, its favorable selection estimate would likely decrease.”

HLC Analysis: https://www.hlc.org/wp-content/uploads/2025/10/HLC-MedPAC-Report_.pdf

#medicareadvantage #overpayments #riskadjustment #cms #medpac #congress

— Marc S. Ryan